Endowus CashUp portfolios, which consist of money market and/or short-duration fixed income funds (unit trusts), are designed to deliver relatively stable returns compared to other fixed income portfolios of longer durations & maturities. Nevertheless, there are risks in investing in these portfolios and they are not capital-guaranteed.

The return potential of each Endowus CashUp portfolio is positively correlated to the risk profile of the underlying investments. For example, Endowus CashUp Plus takes more duration and credit risk in exchange for higher return potential, followed by Endowus CashUp Simple. Simply put, bond duration is a measurement of interest rate risk.

- Bond prices and interest rates move in opposite directions. If interest rates rise, bond prices will likely fall, and vice versa.

- Longer term bonds are more sensitive to interest rate changes than bonds with shorter maturity dates.

To further understand how bonds work, please kindly refer to https://endowus.com/en-hk/insights/why-invest-bonds

The higher risk taken by Plus in a normal environment does and has provided more upside to the portfolios than Simple, but at the same time, it subjects these products to higher volatility to achieve that higher return. It is therefore important for clients to choose the portfolio based on their goals (i.e what they intend to use the funds for), expected returns, drawdowns that they are willing to withstand in the worst case scenario and their preferred holding time horizon.

Let's take an example - money that would be required for an important medical expense or housing down payment in the very near future is more suited for an investment in Endowus CashUp Simple, as compared to Endowus CashUp Plus. This is because the primary objective is more likely to be capital preservation, rather than chasing after higher return/yield.

What are the risk considerations for investing in Endowus CashUp portfolios?

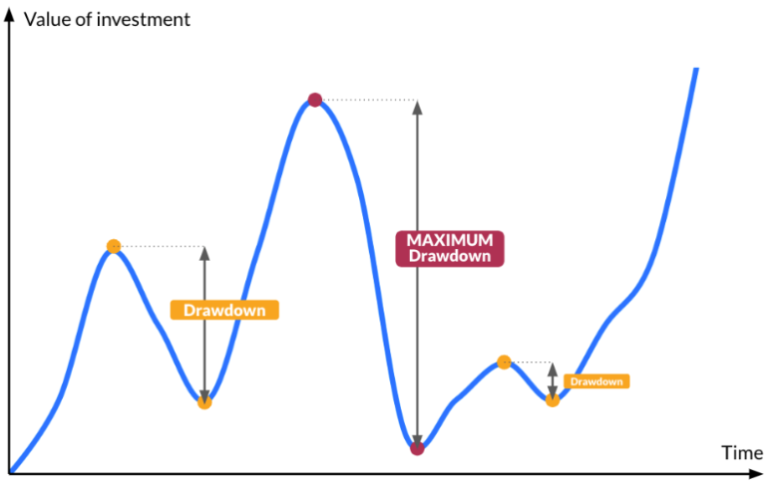

Understanding the historical maximum loss of the respective portfolio can be a good way to assess whether the portfolio is suitable for your risk appetite.

Historical maximum loss(“drawdown”) is the fall from the peak (the highest point) to trough (the lowest point) in investment value, based on historical performance.

Investors may use the historical maximum drawdown as an indication of the maximum loss they may have experienced by investing in the specific portfolio over a period of time. Do note that this maximum loss may or may not be "realised" or "booked", depending on whether or not the investor cuts his/her losses and sells at the bottom.

Please also note that the drawdown figure is based on historical performance, which may not be indicative of future performance. There is always the risk that the latest/existing maximum drawdown will be overtaken by a new maximum drawdown in the future. Investors should therefore view the historical maximum drawdown as a reference point and not a guarantee of future maximum loss.

In calculating the probability of the portfolios achieving their intended goals, we closely monitor their performances over the different time periods. We also look at the maximum drawdown in the past, such as in March 2020, and the long and gradual pullback between 3Q 2021 to 2Q 2022. However, past performance can only be a reference for future returns and not a guarantee of future returns.

You should select a Endowus CashUp portfolio based on your unique financial circumstances, as discussed above. If you need help in selecting a suitable portfolio for your needs, please contact our SFC-licensed advisors via email, Whatsapp, or an advisory call via https://endowus.com/en-hk/contact-us.